Patrocinado

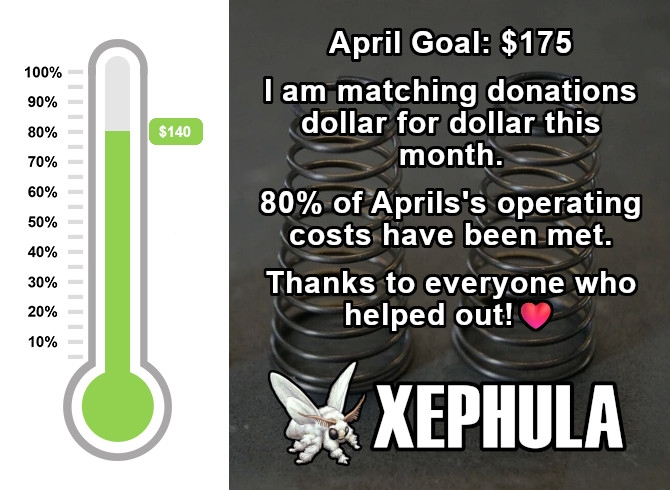

We are, so far, 80% funded for April. I am matching donations dollar for dollar this month. Thanks to everyone who helped out. 🥰

Xephula monthly operating expenses for 2024 - Server: $143/month - Backup Software: $6/month - Object Storage: $6/month - SMTP Service: $10/month - Stripe Processing Fees: ~$10/month - Total: $175/month

Patrocinado

Quick Ships From Midwest • Trusted Source • High Quality Construction • Satisfaction Guaranteed

Read the full article at https://lnkd.in/dgyYKHWv and see the full video at https://lnkd.in/dicbHm6u and at https://lnkd.in/dmzR36QA and at https://zalma.com/blog plus more than 4000 posts.

The United States District Court for the Southern District of Mississippi, Southern Division, entered an important decision with regard to water damage and insurance policy coverages raised after Hurricane Katrina.

In Leonard v. Nationwide Mutual Insurance Co., 499 F.3d 419 (5th Cir. 08/30/2007), the first of the Katrina cases to go to trial, the court found that the Leonards’ residence was not covered by any policy of flood insurance at the time of the storm. Flood insurance is available to anyone, regardless of which flood zone their residence is situated in, yet the plaintiffs did not purchase it; they purchased only a common homeowner’s policy from Nationwide.

Because the adjective “physical” is defined as “having material existence,” mold spores undoubtedly have a “material existence” even though they are not tangible or perceptible to the naked eye. Therefore, mold contamination constitutes a “physical loss” within the meaning of a policy and, assuming all other policy conditions are met, the cost of removing mold from a property, or of replacing personal property, may be recovered under a property policy. The Fifth Circuit found, however, that the anticoncurrent cause exclusion was enforceable and reversed the part of the trial court decision determining the exclusion did not apply.

Under Mississippi law, the judge concluded that where there is damage caused by “both wind and rain (covered losses) and water (losses excluded from coverage) the amount payable under the insurance policy becomes a question of which is the proximate cause of the loss.” This is, of course, subject to the evidence presented at trial.

ZALMA OPINION

Whether a claim is for water damage, wind damage, or resulting mold infestations as a result of water infestation it is important that the insurer conduct a thorough investigation into the causes, determine which are due to a covered peril and those which are clearly and unambiguously excluded by the policy. The video discusses the types of decisions that are rendered by the courts after a catastrophe like a hurricane.

(c) 2021 Barry Zalma