Appraisers Can't etermine Causation

Appraisal Limited to Quantum of Crop Loss

Read the full article at https://lnkd.in/gQ_WNKAP and see the full video at https://lnkd.in/gctnSsXS and at https://lnkd.in/gRfe9FR5 and at https://zalma.com/blog plus more than 4350 posts.

In Agrisompo North America, Inc. v. Coldwater Planting Company, M&W Farms, LLC, Brazil Planting Company, Pushen & Pullen Farms, and Webb Farms, No. 3:22cv51-MPM-RP, United States District Court, N.D. Mississippi (November 4, 2022) Coldwater Planting Company, et al moved to dismiss this action.

ISSUES

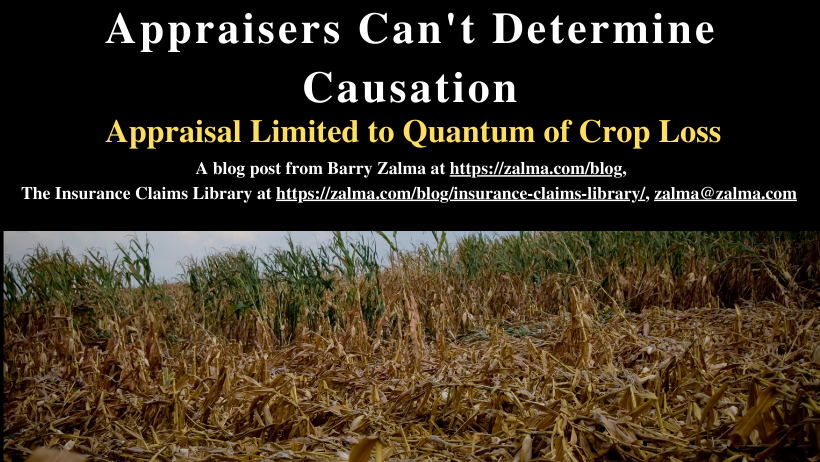

Plaintiff Agrisompo asked the USDC to enter an order appointing an “umpire” to decide the underlying crop insurance dispute. The dispute was to determine whether the crop damage suffered by the insureds in June 2021 was caused by a covered wind damage event or a non-covered flood event.

The parties were unable to resolve their disagreements regarding this issue, and plaintiff responded to the impasse by suing to appoint an umpire. Plaintiff contended that the court has the authority to make such an appointment based on an appraisal policy provision which states that the appraisal procedure will be used “[i]f you and we fail to agree on the percentage of loss caused by one of the insured perils ....”

ANALYSIS

There is extensive Mississippi authority holding that, under the law of this state, an appraiser may not determine causation issues under an insurance contract. In Jefferson Davis Cnty. Sch. Dist. v. RSUI Indem. Co., 2009 WL 367688, at *2 (S.D.Miss. Feb. 11, 2009), Judge Parker wrote that: “Defendant argues that appraisal is inappropriate because this case involves ‘coverage and causation questions, not a dispute about the value of an admittedly covered loss.’”

Judge Parker also wrote that “it is clear that under Mississippi law the purpose of an appraisal is not to determine the cause of loss or coverage under an insurance policy; rather, it is ‘limited to the function of determining the money value of the property' at issue.” (emphasis added)

This authority convinced the USDC as being directly on point, and, in response, plaintiff is only able to offer it precedent from other states, which follow a different interpretation of the law. While plaintiff is able to cite extensive authority from other jurisdictions in this regard, this merely serves to highlight the fact that it is defendants who are able to offer Mississippi precedent on point.

Plaintiff did not dispute that the diversity action is governed by Mississippi law, and it therefore seemed clear to the court that the relief which it sought from the court is unavailable to it. The court noted that a civil action is presently pending in the Greenville Division which seeks to litigate the insurance coverage issues. Therefore the court concluded that that case is the proper forum for the parties to resolve their disputes.

Defendants' motion to dismiss this action was, therefore, granted.

ZALMA OPINION

Standard "appraisal" language limits the ability of the appraisers to only determine the amount of loss. Determination of coverage disputes can only be resolved in appropriate breach of contract action. Some jurisdictions have tried to give appraisers more authority than that provided by the policy. The USDC kept to the authority in the policy and followed by the state of Mississippi.

(c) 2022 Barry Zalma & ClaimSchool, Inc.

Barry Zalma, Esq., CFE, now limits his practice to service as an insurance consultant specializing in insurance coverage, insurance claims handling, insurance bad faith and insurance fraud almost equally for insurers and policyholders. He practiced law in California for more than 44 years as an insurance coverage and claims handling lawyer and more than 54 years in the insurance business. He is available at http://www.zalma.com and [email protected] and receive videos limited to subscribers of Excellence in Claims Handling at locals.com https://zalmaoninsurance.locals.com/subscribe.Subscribe to Excellence in Claims Handling at https://barryzalma.substack.com/welcome.

Write to Mr. Zalma at [email protected]; http://www.zalma.com; http://zalma.com/blog; daily articles are published at https://zalma.substack.com. Go to the podcast Zalma On Insurance at https://anchor.fm/barry-zalma; Follow Mr. Zalma on Twitter at https://twitter.com/bzalma; Go to Barry Zalma videos at Rumble.com at https://rumble.com/c/c-262921; Go to Barry Zalma on YouTube- https://www.youtube.com/channel/UCysiZklEtxZsSF9DfC0Expg; Go to the Insurance Claims Library – https://zalma.com/blog/insurance-claims-library

We are 100% funded for October.

Thanks to everyone who helped out. 🥰

Xephula monthly operating expenses for 2024 - Server: $143/month - Backup Software: $6/month - Object Storage: $6/month - SMTP Service: $10/month - Stripe Processing Fees: ~$10/month - Total: $175/month